I. Introduction

1. Background and aims of the study

The Korean construction industry has been expanding its scale of international contracts while performing major roles in national development during each difficult economic period since its entry into the international market in 1965. Because overseas market entry of the Korean construction industry has helped national growth, each new government has established policies for overseas construction market entry. As a result of such efforts, the Korean construction industry is close to achieving a yearly contract volume of around 70 billion USD, with approximately 8% of the international market share.

However, despite such outstanding achievements, the status of overseas market entry of the Korean construction industry is limited in the types (mostly plants) of construction and areas (mostly the Middle East) of operation as well as a decreasing share of the international housing construction market. The Korean construction industry, in contrast with the Japanese construction industry, actively searches for overseas market entry when the domestic construction market becomes unsound. Recently, the Korean construction industry has shifted its interest to the overseas construction market because of a stagnating domestic market. However, the forecast indicates that overseas market entry will become more difficult due to recent low oil prices, industry struggles to produce breakthroughs, market diversification, and the expansion of construction types.

Growth in world population and inflows of population into cities have caused housing shortages and resulted in the additional development of new cities. Most overseas apartments are considered to be related to such new city developments. World public institution statistics indicate forecasts of 70% urbanization and a 2.9-billion increase in population in cities worldwide by 2050. Such a rate of growth requires the construction of about 9,150 new cities the size of Dong-tan New City in Korea. 90% of the new cities will be constructed in China and in Southeast Asian countries. It is noted that China is currently constructing or planning about 150 new cities. Such newly built cities and buildings typically exhibit the global trend of “sustainability.”

The Korean construction industry requires new designs and strategies to enter active housing construction markets throughout the world. Such needs share the context of the previously mentioned diversification of construction types and areas. The authors of this study consider the technology and system of “cost-saving long-life housing,” recently studied for national policy, as such a new strategy. Moreover, the authors believe that a review of the external environment of each country is imperative.

Therefore, this study aims to analyze the external environment of each prospective country (classified according to the market type) for the entry of long-life housing through CAGE1) analysis. It also evaluates the list of top countries where the Korean construction industry is already active. The result is will be utilized as part of the data for determining the overseas market entry of long-life housing in the future.

2. Methods of the study

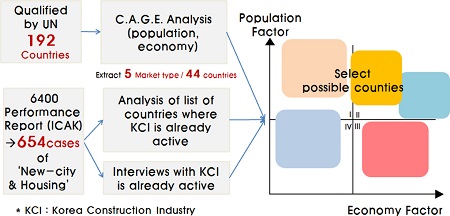

To determine the possible countries, CAGE analysis and a list of the top countries where the Korean construction industry is already active were used.

First, 44 countries were classified into five market groups on quadrants, with the two coordinate axes (population, economy) drawn from CAGE analysis. Second, the top 10 countries with existing Korean construction industry involvement were determined, with 654 cases of international construction performance selected through keywords related to “new city and housing” from 6400 performance reports (2.4.1990- 12.24.2013) of the International Contractors Association of Korea. Third, the external environments of five of the 10 selected countries that may influence the entry of long-life housing were analyzed.

For the data on the external environment of countries that are possible markets, related online and offline documents in Korea and interviews with experts and people with overseas residency experience were compiled as the spatial component, whereas related data limited to the recent two years were collected as the temporal component to find the most updated trend.

II. Previous Literature Review

1. Trend of study on the overseas market entry of the Korean construction industry

“Study on Strategies utilizing u-City for the Overseas New City Market Entrance” (2007) by Korea Institute of Civil Engineering and Building Technology (KICT) portrays the u- City construction projects that have been successively implemented in Korea as new export products for the current trend of increasing entry of Korean constructors into overseas markets. This growing trend is a result of growth in real estate and new city developments overseas, and the study presents strategies and various support measures for overseas market entry of u- City construction. The domestic and overseas performance status and forecast related to new city and u-City are analyzed for this purpose. Based on the analysis result, guidelines for future entry into new city development projects utilizing u- City will be prepared by establishing and presenting basic and detailed strategies. The study encompasses the analyses of the market, technology, and requirements for the practice as well as the investigation of expert opinions.

“Trend of Studies on the International Market Entrance of Korean Construction Industry” (2014) by J. Chung organizes the previous literature present in the websites of Architecture and Urban Research Institute, Civil Engineering Research Information Center, National Assembly Library, and International Contractors Association of Korea by using the keywords “overseas market entry+construction industry or Korean constructors.” It also analyzes research reports, academic theses, academic presentations, and contributions with the major policies in the same time periods, given that the trend analyses on temporal researches of overseas market entry have been insufficient. According to the analyses results, research reports and contributions demonstrate relations between policy status and literature keywords. Most literature presents vitalization measures and competitiveness reinforcement measures for the construction sector as conclusions and yet fails to show major temporal differences. In particular, “localization” and “local customization” are frequently mentioned, whereas specific details are insufficient. The study notes that for future overseas entry strategies and research to vitalize long-life housing distribution, efforts to develop specific concepts of “localization” or “local customization” are required, and the establishment of a selection criteria for the possible countries and the analyses of each country’s external environment are necessary to handle the housing construction area.

2. Trend of study on apartments in china, southeast asia, and the middle east by Korean researchers

N. Lim’s “Analysis on the Plan Types of Small and Middle Sized Apartments in Beijing, China” (2012) attempts to study the compositions and characteristics of small- and middlesized apartments resided in or sold during 2009-2012 in Beijing for the smooth distribution of small- and middle- sized apartment planning. The analysis presents the following characteristics of unit planning of small- and middle-sized apartments in China: (1) the separation principle between open and private spaces is displayed strongly such that open areas such as living rooms and kitchens are arranged close to entrances, and bedrooms are placed inside, far from the entrance but close to bathrooms; (2) LD-K type is most frequent, so the living room and dining space are the most open areas and form important places where families gather; and (3) many plans display direct connections from the entrance to the living room.

D. Hoang’s “Comparative Study between the Spatial Compositions of High-rising Apartments in Vietnam and Korea” (2011) attempts to find reference data for Korean architects who design apartments in Vietnam by evaluating the differences found from the analysis and comparison between the spatial compositions of high-rise apartments in Vietnam and Korea. Through the literature and questionnaire investigation, the study presents the irrationalities and advantages in Korean apartment plans for the Vietnamese market based on comparison and analysis results.

“Study on the Guideline Development of Unit Plan for Iraqi Apartments Applying the Pattern Language of Christopher Alexander” (2014) by J. Choi (currently conducting the national policy research of “Development of Construction Prototype of each Local for the Overseas Market Entry of Apartment Industry”) addresses the fact that the Iraqi government actively promotes apartment construction to increase the housing rate (while international contractors have obtained contracts, Korean constructors are still considering entry into the country) and discusses the lack of data in Korean research on apartment plans that reflect the residential culture of Iraq. The study proves that planning new residential formations that reflect local residential culture is possible by classifying the residential culture. Planning of residential space in Iraq through pattern language can be grouped into four categories: (1) protection of visual privacy, (2) climate characteristics, (3) spatial composition of Iraqi housing, and (4) size and characteristics of Iraqi families. A total of 34 patterns were selected from the pattern language for the application of Iraqi residential culture to the apartment unit plan. Based on the 34 selected patterns, the study presents guidelines for plans of space composition, formation, entrance, external walls and windows, and external spaces for the apartment unit.

III. Selection of Possible Countries for Long-life Housing

1. Possible market group selection through CAGE analysis

The CAGE framework was selected as the base for the overseas market entry of long-life housing.

CAGE is a practically and frequently used measure for analyzing the limits of overseas market entry and identifying countries with relatively easy entry based on differences in culture, administration (politics), geography, and economy.

This study uses CAGE to determine the possible market groups based on the administrative, geographic, and cultural factors by classifying markets on the basis of economic and demographic elements of the housing markets.

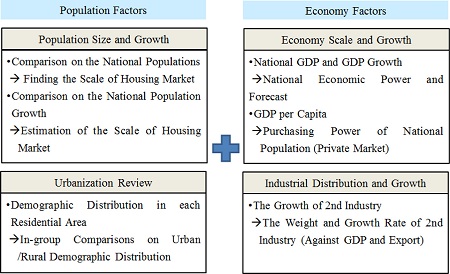

Data from the UN, OECD, and IMF are utilized for objective comparisons between countries.

Based on the general fact that countries having more population, higher population growth rates, and greater national economic power (national GDP, GDP growth, GDP per capita, etc.) receive greater shares of the overall demand for housing, the attractiveness of the housing market for each country in the world is measured using population and economic variables. Then, the market groups for possible entry are divided broadly as follows.

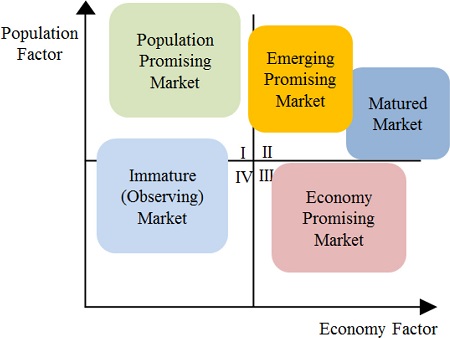

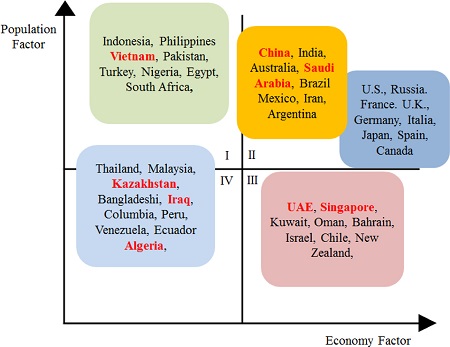

A population promising market (I in Figure 3) represents a market where the economic power of the country is insufficient, yet large-scale complexes including new cities can be established in the future according to urbanization plans backed by rapid population growth. Although the economic scale is insufficient, these markets are expected to experience high population growth, thus forming high possibilities for future new city development. Therefore, these markets can be deemed viable for entry by the Korean construction industry.

An advanced market (II) has been initially determined to be somewhat ambiguous for entry by the Korean construction industry since local and advanced countries’ constructors are already in play. However, both the scale and purchasing power of the housing market are established. Such a scene appears because the advanced market combines two characteristics: one from the matured market-slower population and economic growth-and the other from the emerging market-future growth based on certain scales of population and economic size.

An economy promising market (III) has high demand for new housing development or housing replacement due to continuous and future economic growth despite insufficient population size or population growth. Therefore, this market is determined to be an easy entry option for the Korean construction industry.

An immature market (IV) includes markets of countries for which it is difficult to forecast any short-term growth in the housing market due to insufficient economic and population factors; however, entry may be possible due to future changes in the market environment or policy factors. Since the population and economy are still weak, this market should be observed before entry by Korean or any other overseas construction industry.

2. Selection of top 10 Korean constructor-entered countries

Reported data, including the keywords “new city, apartment, housing, residential, and commercial complex,” were searched in 6400 performance reports of the International Contractors Association of Korea to find countries available for the entry of long-life housing among the countries where Korean constructors are already in play.

Residential, city, and other areas were selected for the large classification, and the detailed classifications of each large classification were set. The detail categories include housing, apartment, combined facility, residential complex, combined residential complex, and small apartment for the residential category; new city, city development, city plan, new town, new capital, and city improvement for the city category; and hotel, lodge, resort, condo, dormitory, residence, and officetel for the others category.

There were 654 cases of overseas construction performance under the classification “residential, city, and other,” including 318 cases for residential, 143 for city, and 192 for others.

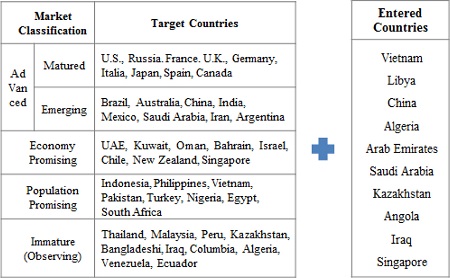

The order of entry frequency by country presents the following sequence: Vietnam, Libya, China, Algeria, Arab Emirates, Saudi Arabia, Kazakhstan, Angola, Iraq, and Singapore.

3. Selection of possible candidate countries (Group)

By organizing lists of the countries included in the target market group determined by CAGE analysis in section 3.1 and the 10 entered countries of section 3.2, candidate groups of possible countries were selected as shown in Fig. 4. Matured markets are mostly comprise advanced countries that have large economies and stable population growth. Emerging promising markets are composed of countries with smaller economies compared with mature countries but allow market entry due to population growth. Matured markets are already advanced for the housing market, since these countries have already achieved development and evaluation of long-life housing technology. This indicates a difference from other market groups for entry. Therefore, it is excluded from this study.

From the nine countries included in the emerging promising market (II) group, China and Saudi Arabia were selected as the countries available for entry of long-life housing, whereas Vietnam was selected from eight countries included in the population promising market (I) group. From the nine countries included in the economy promising market (III) group, the U.A.E. and Singapore were selected, whereas Kazakhstan, Iraq, and Algeria were selected from 10 countries included in the immature market (IV) group.

From these selections, the external environments of countries that seem most promising (China, Vietnam, and the U.A.E.) in the three market groups (excluding the immature [observing] market) were investigated in this study. In addition, East Russia was included in the countries for external environment investigation because expert opinions indicate that although East Russia is slow in development (unlike West Russia) the apartment market has been expanding recently.

IV. External Environment Analysis of Each Possible Candidate Country

1. China

1) Opportunity factors

The GDP per capita of China crossed 5000 USD in 2011, and the country will soon become a middle power. The urbanization rate of China currently is 54% (World Bank, 2014), similar to the level of Korea in the early 1990s. The Chinese government has established Urbanization Promotion and Healthy Development Plans (2011-2020) to drive the urbanization rate to 60% or higher by 2020 and plans to invest 40 trillion CNY (7,200 trillion KRW) for urban construction and low-income housing through 2020. The Xi Jinping administration has particularly adopted domestic consumption stimulation through urbanization as the new growth engine. Moreover, the Chinese government has established a New City Development Policy, and has shown an interest in the expertise from new city developments (Bundang, Ilsan, and others) in Korea.

The Korean construction industry entered the Chinese market, the largest in the world (1.6 billion population and an area of 9,596,961 km2), in late 1990 and ranks tenth in the list of constructors with approximately 670 construction contracts totaling 1.34 billion USD, which is low considering the total trade between the two countries. Recently, Korean-style apartments have been under construction in larger cities due to the “Korean wave” influence. However, Korean contractor entry in the market is still insignificant.

After joining the WTO, housing prices in China have maintained their growth trend despite the government’s suppression policy. Despite its socialist system, China recognizes housing as permanent private property by enforcing the Material Right Law (March 2007).

Some apartments in China are called “Máopîfáng” (“unfinished”) and “Jingjuwangfáng” (“basic interior”). Since such apartments are similar to Korean long-life housing, similar markets for the entry of long-life housing are considered to exist.

China holds the Korea-China Cooperation Conference in City and Housing Areas (9th Event, 2012) jointly with Korea. An MOU between the two nations on the sustainable urban development area has been entered (2013), and the Korea- China Free Trade Agreement (FTA) will be initiated from 2015.

2) Threat Factors

The number one country in terms of international construction contracts, China is home to five of the 10 largest constructors in the world. Although the construction industry is vitalized due to the extensive urbanization policy in the country, only the big picture on urban construction has been drawn (Ministry of Land, Transport and Maritime Affairs, 2010). China is a socialist nation; therefore, closed tendencies often appear. The unique culture called “Guanxi” that exists in China is considered a barrier for foreign constructors, including Korean companies.

Since Chinese companies possess the basic technology while maintaining low pricing, their domestic constructors possibly have an advantage in competition with Korean companies.

2. Vietnam

1) Opportunity factors

With a current GDP per capita of approximately 1,700 KRW (144.6 USD), Vietnam shows rapid population increases, led by Hanoi, Ho Chi Minh City, and other major cities. The urbanization rate of Vietnam is 33% (World Bank, 2014), while the housing distribution rate based on western-style apartments is approximately 10% (Korea Trade-Investment Promotion Agency).

Due to severe housing shortage, the Vietnamese government has declared that supplying social housing is a priority at the national level and is performing 124 construction projects nationwide. Therefore, the country is expected to have high possibilities for development in the next 20 years. Additionally, the supply of apartments for higher classes and foreigners is developed mostly in large cities (e.g., Hanoi and Ho Chi Minh City). Such apartments under construction in Vietnam are of the column structure, which have high ceiling heights with minimum interior finishing. It has been confirmed that the recent “Korean Wave” influence is increasing the attention given to Korean-style apartments in Vietnam as well.

The Vietnamese prefer villa to apartments. The reason for such a residential preference seems to be based on the possible activities of residents in such villa-from changing the internal space arrangement to even moving the outer wall in accordance with “feng shui” and the fortune of each individual resident

Korean, Chinese, and Japanese constructors are active in Vietnam. It has been observed that Chinese constructors are suffering from the influences of an anti-Chinese demonstration (the land dispute between Vietnam and China in May 2014) and Chinese actions prohibiting new investment in Vietnam (retaliation for the dispute in June 2014). On the other hand, Japanese constructors are more interested in railway/road construction than in apartment construction.

The Vietnamese government’s action of “Mitigation of Condition’s for Foreigner’s Housing Purchase” (February 2014) is revitalizing the real estate market. Vietnam is under the cooperation in the real estate and has signed an FTA with Korea.

2) Threat Factors

Like in China, the Political Bureau of the Communist Party enjoys full authority on the entire proceedings in Vietnam; however, the political system is stable.

Unlike other Southeast Asian countries that are influenced by Indian culture, Vietnam is linked to the Chinese character and culture; hence, many Chinese constructors have entered the Vietnamese market.

The technologies used by Vietnamese constructors have reached a certain level that classifies them as having an advantage over Korean companies in price competition.

Therefore, some experts note that the market entry of infill manufacturers would be more promising than that of construction companies for the Korean construction industry, because Vietnamese parts manufacturers are still in a relatively weaker position.

3. United Arab Emirates (the U.A.E.)

1) Opportunity Factors

The U.A.E., which consists of seven emirate states, is renowned as a global oil producer, with a GDP per capita of 44,771 USD (IMF, 2014) and an urbanization rate of 84.4% (CIA World Factbook, 2011). According to BMI, an expert market research institute, the scale of the construction industry in the U.A.E. in 2014 was approximately 3.9 billion USD, exhibiting 5.5% growth over the previous year and accounting for 9.1% of the U.A.E.’s GDP. Abu Dhabi (53%) and Dubai (46%) are the major areas of the U.A.E.’s construction industry the U.A.E. and are central to the U.A.E.’s construction boom. Real estate, including housing and commercial buildings, makes up 58% of the total construction industry in the U.A.E.

According to IMF estimates, the U.A.E.’s population will grow from 5.4 million in 2010 to 6 million in 2015 due to increased inflows of foreigners. Therefore, the inventory of residential and commercial space is expected to increase to accommodate such population growth. Therefore, real estate and infrastructure-related projects under the government’s administration are expected to be continuously offered. Various housing projects are being developed in Abu Dhabi and Dubai based on Plan Abu Dhabi 2030: Urban Structure Framework Plan (central city development plan) and the Dubai Strategic Plan 2015 (Dubai Economic Development Plan). In addition, city development projects for the northern Emirates trail behind in development in comparison to Dubai and Abu Dhabi, even with active development plans. A plan to construct adequately priced apartments (affordable housing) for low-income foreign workers has been announced, and the construction of housing to accommodate 380,000 workers is in progress. Moreover, the U.A.E. government is performing various housing-related supporting projects, such as the Zayed Housing Programme for life stability through continuous housing supplies, as part of efforts to improve the living environments of citizens.

Since demands for real estate and construction are increasing, the Dubai government has promoted an environment-friendly and green economy.

2) Threat Factors

Middle Eastern countries consider local construction performance important. Moreover, performance records from various construction projects are required in order to secure new opportunities and compete for future large-scale projects or projects in other Middle Eastern countries. The scale of general construction projects is smaller than it is for oil or gas plant projects and generates an insignificant return on investment. However, from a long-term perspective, such small-scale construction can be considered an opportunity for construction companies entering the Middle Eastern construction market for the first time. However, local constructors possess advantages in contracting for general construction projects, such that even a single contract for a Korean constructor is, in fact, difficult to secure. Therefore, business cooperation, such as joint participation with a local constructor, establishment of a local company, or continuous networking with a local company, could be required.

Dubai had been maintaining the Zone 2A Seismic Code Policy even though the country is safe from earthquakes. However, considering recent large earthquakes in Iran, Pakistan, and other places, the country conditionally raised the policy to Zone 2B. Since the determination was made without any announcement on enforcement, the industry is facing confusion regarding regulations. Since the determination is applied especially to buildings currently under construction, issues of redesign, reanalysis, and supply of new construction materials (seismic endurant) are faced. Any Korean company either involved or attempting to promote construction projects in Dubai should acquire an accurate understanding of and prepare for Dubai’s seismic code in advance.

In general, the housing type in the U.A.E. is detached and not apartment units because of the country’s vast amount of land. Each housing unit is large (496 m2 or larger) and is provided for free, so the entry of long-life housing as an alternative housing type is expected to be difficult.

4. East Russia (Khabarovsk)

1) Opportunity factors

Russia, the world’s ninth-ranked country in terms of GDP (2.573 billion USD [2014, IMF]), exhibits numerous differences from the West, which is already developed, and the East, which is still in need of development. The urbanization rate of Russia is 73.8% (2011). This study is limited to Khabarovsk in East Russia.

The country exhibits severe disparity between the rich and poor and faces economic issues like high prices with low average wage. Russians use their wages for living costs only and typically have no savings. Since education and medical care are free, low wages are not a considerable financial problem in terms of living conditions. People show little desire to increase their wealth, and they want relaxed lifestyles.

With land available under long-term rent for 50 years, the complete process from design to sales can be performed. A sales prices fluctuation is applied for private housing construction and sales include the concept of construction investment partnerships. Since the financing system is inadequate, construction is performed with some payments from future residents. Therefore, the construction period is very extensive, with a tendency of sales rate increasing right before completion.

In general, apartments in five- to ten-floor buildings are supplied to public officers and soldiers free. Since apartments are bequeathed to children, the desire for ownership or investment in housing is rather low, and the characteristic of staying long-term in the same location is also evident.

For local apartments, the constructor completes only the structure and outer wall, and the resident directly completes the interior walls and finishing by purchasing desired materials. The upper-income class prefers European materials, and the low- and middle-income classes use Chinese materials.

Other than local constructors, almost no competitors exist. Although some Chinese constructors appear in the market, the possibility of Korean constructors competing within the proposed period needs to be highly evaluated.

2) Threat Factors

Since the partially improved older Soviet technology standard (and not the global US technology standard) is applied, materials and equipment are frequently supplied from the local market. Insulation, moisture, structural standards, fire, evacuation, ventilation standards, and sunlight and setback regulations are especially strong.

Because of the Russian trend of avoiding the purchase of middle-class materials between expensive European and Japanese materials and cheap Chinese materials, the export of Korean materials is very difficult.

V. Conclusion

We selected the possible countries for the overseas expansion of long-life housing by making a comparison between the possible market country groups list and the top 10 entryexperienced country lists for Korean constructors. Then, the opportunity factors and threat factors for overseas expansion of long-life housing in each country were studied. The results from these activities are as follows.

First, based on the general fact that countries having larger populations, population growth rates, and national economic power (national GDP, GDP growth, GDP per capita, etc.) have the greatest demand in housing, the attraction of the housing market for each country in the world was measured with population and economic variables. The possible market groups were classified as population promising markets (eight countries), advanced markets (eight emerging promising markets countries and nine matured markets countries), economy promising markets (nine countries), and immature markets (ten countries).

Second, Vietnam, Libya, China, Algeria, the U.A.E., Saudi Arabia, Kazakhstan, Angola, Iraq, and Singapore were identified as the top countries with existing involvement of the Korean construction industry in housing and city areas. Vietnam is a population promising market, the U.A.E. and Singapore are economy promising markets, and China and Saudi Arabia are emerging promising markets. They were selected as possible candidate countries by comparing the countries in the possible market groups. Kazakhstan, Iraq, and Algeria are immature markets.

Third, the findings of opportunity factors on the entry of long-life housing in four countries (Vietnam, the U.A.E., and China in the market groups and Khabarovsk, East Russia, from the interview investigation) presented the following results: (1) four countries have housing demand that is increasing or that is expected to increase in the future, and apartments are generalized in those countries (excluding the U.A.E.); (2) the common feature of apartments in the three countries (excluding the U.A.E.) is either the column or combined type, and infill is completed by residents separately from overall building construction; and (3) Vietnam and China share common characteristics since they are being systematically opened for entry due to intergovernment agreements or conventions. The findings for threat factors were as follows: (1) socialist nations (China, Vietnam, and East Russia) or countries closed to foreign companies (the U.A.E.) make entry for foreign companies difficult; and (2) limits exist on quality and pricing for competition with local companies or foreign constructors that have already entered the market.

Although there is some contention that overseas market entry of long-life housing may be too early, the results of this study confirm that possible external environments are forming in some countries in the world. Construction companies from advanced countries are in fierce competition to maintain the housing development market share. On the other hand, Korean constructors are found to be insignificant in the international housing market because constructors prioritize profit and focus on plant construction and Middle Eastern areas.

Although external environments allowing for overseas expansion are present, threat factors exist. Therefore, the Korean construction industry should hurry with overseas expansion while reviewing detailed local market information. Further, like the numerous countries in the world that are making efforts for overseas market entry through their national construction industry, the Korean government should gravely consider establishing support policies to provide more competitive bidding power for the Korean construction industry before it is too late.